Before I start, I believe it is necessary to disclaim that cheaper stocks are not stress-free to buy and do not necessarily offer a smoother path to profitability than more costly offerings. Nonetheless, it's indisputable that many investors have natural inclinations toward low-priced equities, which are more volatile than their high-priced peers. This naturally higher volatility opens up the possibility of bigger gains in a shorter period of time, however, I advise you to assess your individual risk tolerance and fiscal situation to determine which investing strategy is best for you.

The following five stocks have certain positive fundamentals and share prices trading at or below $5. The usual caveats apply, but these low-cost shares have positive analyst estimates, solid earnings and growth initiatives that make them viable options for the rest of 2013.

1. Sirius Radio - (SIRI)

Current Price: $3.21

The Breakdown

The promulgated satellite service provider recently reached its 52-week high, and as of December 31, 2012, had 23,900,336 subscribers. Although Pandora (P) recently announced a surprising fourth quarter earnings report - sending shares 25% the next day - Sirius has recently announced that it will exclusively launch "South by Southwest Radio," and "Bon Jovi Radio," in the coming weeks, both of which are estimated to bring in an additional 100,000 hours of monthly streaming alone. Sirius' shares have had a decent run so far this year, gaining more than 10%, compared to a gain of more than 5% for the NASDAQ. TheStreet Ratings recently reiterated it as a buy with a rating score of A- and the company's strengths can be seen in multiple areas, such as its revenue growth, solid stock price performance, notable return on equity and expanding profit margins.

Analyst Ratings and Analysis

(Click to enlarge)

(Click to enlarge)

Sirius' gross profit margin is rather extraordinary; currently it is at 63.20% - higher than more than 79% of other companies in the Broadcasting & Cable TV industry, which means it has more cash to spend on business operations as compared to its peers. Furthermore, SIRI's P/E Ratio is lower than 89% of other companies in the Broadcasting & Cable TV industry. Since the same quarter one year prior, revenues rose by 13.9%. This growth in revenue appears to have trickled down to the company's bottom line, improving the earnings per share. Along with this, the net profit margin of 17.50% is above that of the industry average.

Next Earnings Date: May 2nd, 2013

The Bottom Line

The problem of consistent profitability remains a weight on shares, but it's important to understand that revenue continues to climb - this is hardly a company with its best days behind it in 2012. In the coming months, keep an eye out for the rising competition between Pandora and Sirius, but with excellent operating ratios, an increase in annual revenue, and monthly-subscribers growing at an all-time rate, Sirius is far from its climax.

2. ValueVision Media- (VVTV)

Current Price: $3.17

The Breakdown

The multichannel electronic retailer recently reported a larger loss for the fourth quarter reflecting a large asset valuation charge, but showed revenue increase of 20 percent - rising from $147.5 million to $177.5 million. ValueVision said after the markets closed Wednesday that its home and beauty businesses did well and its consumer electronics unit recovered from a year earlier.

Analyst Ratings and Analysis

(Click to enlarge)

(Click to enlarge)

(Click to enlarge)

MarktEdge, Smart Consensus and Thomson Reuters are all specifying positive growth and strong buy signals. The Moving Average Convergence Divergence (MACD) also shows a strong buy signal. VVTV's Gross Margin is more than 83% of other companies in the Retail (Department & Discount) industry, has an EPS Growth Rate greater than 95% of its peers, and is proving to be one of the fastest growing electronic retailers in the industry. In January of 2013, there was some significant insider activity as Keith Stewart (CEO), Sean Orr (Director), and Joseph Berardino (Director) purchased more than 154,000 shares for a combined market value of $337,000.

The Bottom Line

Although ValueVision had a loss and missed Wall Street's expectations, the electronics retailer beat the revenue expectation and is a positive sign to shareholders seeking high growth out of the company.

3.Global Ship Lease - (GSL)

Current Price: $3.62

The Breakdown

When fears about the global economy set in, shipping companies take a big hit, but with the recent news of the Dow reaching its all-time high and signs of an improving market, those fears begin to recede. A company reaping the benefits of this example is Global Ship Lease. The company owns a fleet of modern containerships coming in a range of sizes. The entity's business is to charter out its fleet under long-term, fixed-rate charters to container shipping companies. It is the third largest operator of containerships with a fleet of 400 vessels, with 17 vessels of its own and was spun off from the world's third largest container shipping group, a French company called CMA CGM, back in late 2007. When the financial crisis of 2007 came about, shipping rates plunged, reducing the estimated value of Global Ship Lease boats. Since they are collateral against loans, GSL lenders demanded more money back. GSL was forced to eliminate its dividend, and the stock tanked -- to current levels of around $3.62 from $8. Steven Schuster, a deep-value investor and a portfolio manager who owns a big position in this stock at Bridge Street Asset Management, thinks this little shipper could triple in value over the next few years.

Analyst Rating and Analysis

(Click to enlarge)

(Click to enlarge)

GSL's Gross Margin of 70.95% - more than 75% of other companies in the Water Transportation industry. It also has an excellent net profit margin of nearly 23%. The Return on Equity for GSL of 10.17% shows that it is able to reinvest its earnings more efficiently than 82% of its peers in the industry. While most companies are barely scratching by, GSL has high charter percentages locked in for the next half decade.

Next Earnings Date: March 11, 2013

The Bottom Line

GSL has proven that dry-docking is not a problem with GSL having fleet utilization greater than 98% for any given year. It's hard to pass up a company with its debt easily manageable, a price to book ratio of 0.55, excellent management, and preemptive advantages with CMA CGM that controls much of the market share in the industry. With the market is improving and CMA having a controlling interest in GSL (it owns 45% of the stock) it would not be shocking if this stock moved back up to the $8-$10 range.

4.1-800-FLOWERS.COM, Inc. - (FLWS)

Current Price: $4.90

The Breakdown

1-800-FLOWERS.COM, Inc. is the world's leading florist and gift shop. For more than 30 years, the company has delivered fresh flowers and a selection of plants, gift baskets, gourmet foods, confections, candles, balloons and plush stuffed animals. The florist retailer has nearly 40 million unique customers served by the company's 2,200 employees. 1-800- Flowers.com also recently launched a smartphone app that handles expedited mobile payment.

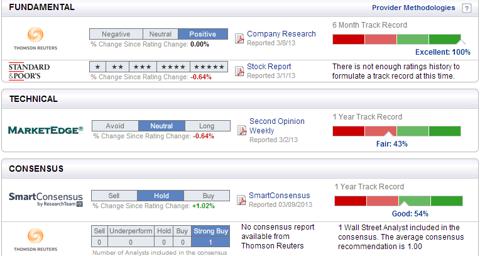

Analyst Rating and Estimates

(Click to enlarge)

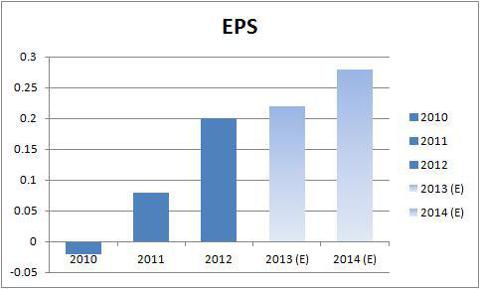

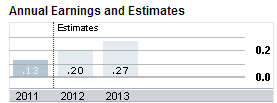

With "Buy" ratings from MarketEdge and Smart Consensus, 1-800-Flowers.com is in a position to continue its growth for the duration of 2013. Multiple growth initiatives are under way, including Merchandising and marketing ingenuity featuring truly original products that have helped drive increased average order value and gross profit margins, focusing efforts in manufacturing, sourcing and shipping that have helped absorb rising commodity and fuel costs and the aforementioned social media program. Analyst estimates also predict a dramatic increase in EPS in subsequent years, as shown by the graph above.

Next Earnings Date: April 30, 2013

The Bottom Line

Although 1-800-Flowers. Com faced noteworthy hindrances in 2008 due to the decrease in discretionary spending, the florist and gift shop guru still has tremendous upside and growth potential with the market reaching new heights. Management has continually renewed its business model to keep up with the ever-changing market conditions, has cut costs, and continues to grow revenue which makes it an appetizing stock to watch.

5. Century Casino's Inc. - (CNTY)

Current Price: $2.97

The Breakdown

Century Casinos, Inc. is an international casino entertainment company, which develops and operates gaming establishments and related lodging and restaurant and entertainment facilities. The company also holds a 33.3% ownership interest in and actively participates in the management of Casinos Poland Ltd (CPL), the owner and operator of four casinos throughout Poland. On November 07, 2012, Century Casinos reported its 3Q financial results. In the report, Erwin Haitzmann and Peter Hoetzinger, Co-Chief Executive Officers of Century Casinos said:

"We are pleased to report another quarter with growth in revenue. All our properties posted solid results in the third quarter, with the single exception of Calgary, Canada. Even though that casino saw table drop increase significantly, by 58%, and also slot coin-in by 8%, lower hold percentages as well as a decrease in food and beverage and bowling revenues, coupled with higher marketing costs, led to a decline in Adjusted EBITDA at the property. Nevertheless, we are optimistic about the Calgary market and are focusing on implementing changes that will raise guests' gaming experience and promote further operating efficiencies to improve the results at our property in Calgary. We are pleased to announce the potential purchase of an additional 33% share of Casinos Poland Ltd and we continue to actively pursue domestic and international casino opportunities."

The 40% upside potential based on the consensus mean target price of $4.02 and the fact that the stock is in an uptrend are all factors that make CNTY stock quite attractive.

Analyst Ratings and Analysis

(Click to enlarge)

(Click to enlarge)

(Click to enlarge)

Century Casino's has a price-to-book value of .61, very low debt-to equity (.03) and a gross margin of nearly 50%. It continues to increase its revenue every year, depicted in the image above. Even during the 2007-2009 economic collapse, Century Casino's proved to have a sustainable business model that could react to market inflation.

Next Earnings Date: April 1st, 2013

The Bottom Line

With an average annual earnings growth of 6.31% over the past five years, low debt to equity, strong growth prospects and trading within eight percent of its 52 week high, Century Casino's is a solid option for an investor looking for a steal.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source: http://seekingalpha.com/article/1262601-5-under-5-stocks-you-should-consider-for-2013?source=feed

tiger woods masters 2012 nikki haley stan van gundy navy jet crash virginia beach crash stephen hawking marion barry

কোন মন্তব্য নেই:

একটি মন্তব্য পোস্ট করুন